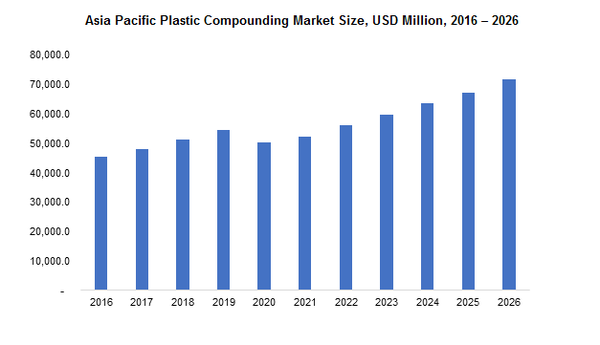

Asia Pacific Plastic Compounding Market Share was USD 54.5 billion in 2019 and will grow at a CAGR of more than 6.1% up to 2026. Plastics compounders enhance the performance of plastic resins with key additives to meet the end-user industry needs. Plastic compounders hold key material knowledge; for instance, bio-resorbable rates, elasticity, security tagging, colour, and a host of other properties of plastic resins that can change for compounding. Modernization of the plastic industry will hold a strong potential for the market over the forecast timeframe. The COVID-19 pandemic has disrupted the supply chain of the Asia Pacific market. It can be majorly ascribed to a decline in product consumption in the major end-use sectors including consumer goods, electrical & electronics, construction, automotive, and aerospace. The Asia Pacific is the largest market in the global plastic compounding industry. Though China has entered the recovery phase in the current pandemic scenario, normalization of full-capacity operations will be delayed majorly due to the halt on international trades. The other major countries in the region including Japan and India will witness sluggish growth in plastic demand in the short-term. However, the market is expected to take its normal course in the coming years. Based on product, the thermoplastic polymer was the largest revenue-generating segment in 2019 and is projected to grow at a CAGR of over 6% during the assessment period. Thermoplastic polymers are widely used across various industries, especially in weight-critical applications. Among the various thermoplastic polymers, polyvinyl chloride was the largest segment with a market share of over 60% in 2019. PVC is widely used in the construction industry in applications such as piping, plumbing, window brackets, and cable insulation, among others. Based on end-user, automotive held the largest market share closely followed by the consumer goods segment in 2019. Plastic applications in automotive components range from windshields to drive systems. Regulations on vehicular weight reduction have been the primary driving force for rising consumption. Automobile giants aiming to achieve weight reduction are reducing their dependency on metal parts and are relying on plastic components. Key players in the Asia Pacific industry include MRC Polymers, Inc., BASF SE, The Dow Chemical Company, Solvay S.A., LyondellBasell Industries, Lanxess Kraton Corporation, A. Schulman, Aurora Plastics LLC, Foster Corporation, Saudi Basic Industries Corporation (SABIC), Asahi Kasei Plastics, RTP Company, Kuraray Plastics, Covestro AG, Chevron Phillips Chemical Company LLC, and PolyOne Corporation. Source:https://www.graphicalresearch.com/industry-insights/1600/asia-pacific-plastic-compounding-market